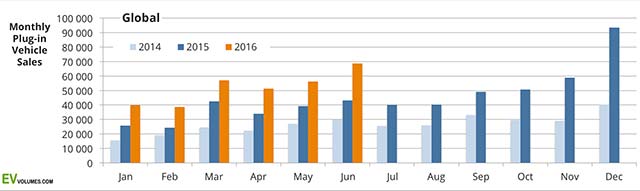

Worldwide plug-in vehicle sales including June were 312 000, 49 % higher than for the same period in 2015. These include all global BEV and PHEV passenger cars sales and light commercial vehicle in Europe.

The total vehicle market is up by 5 % in the first half year to 35 million cars and 12 million trucks. Plug-in vehicle sales grow 10 times faster than the overall market, but still capture a world market share of below 1 %.

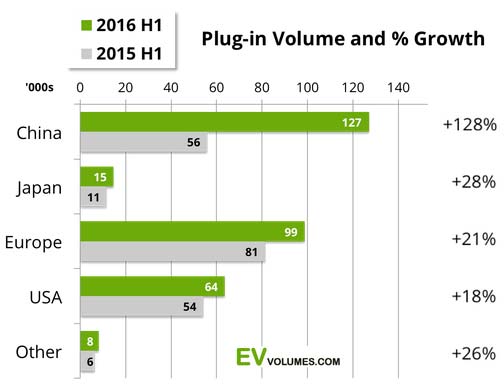

China is the main driver of high growth in Plug-ins and China is increasing its significance as a market and as manufacturing base for “New Energy Vehicles”, the Chinese term for electrically chargeable vehicles. With current regional growth rates, China will stand for 50 % of plug-in sales by the end of the year.

China sets the pace

China is the growth motor for plug-in sales. “New Energy Vehicle” volume for passenger cars more than doubled in the first quarter and growth accelerated to 140 % for Q2. 128 % growth for H1 is much more than in any other region, but the days of 2- or 3-fold sales increases seen in 2014-2015 are probably over.

The US has recovered from the weak development during 2015 (-4 %), posts +19 % for the first quarter and +18 % for Q2. June and July were particularly strong with 50 % more sales than in 2015, Tesla, GM and Ford being the main source of the increase.

Europe struggles to continue on the 99 % growth rate of last year. Many markets develop strong, but the incentive changes for PHEV in the Netherlands and EVs in Denmark darken the overall picture. Growth was 31 % in Q2, but only 13 % in Q2.

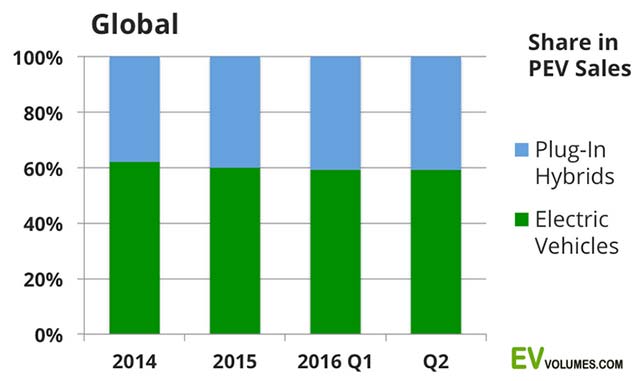

Stable 60:40 Ratio

The mix of battery electric vehicles (BEV) and plug-in hybrids (PHEV) appears to be quite stable. There are differences between the regions, though. In China, the ratio is still two EVs on one PHEV. In USA and Europe, the EV/PHEV mix is approaching a 50:50 split. New model launches, mostly PHEV in Europe/US and mostly EVs in China play an important part in this.

Europe in particular shows diverse and interesting developments in the individual countries, largely depending on the tax & incentive structures and domestic product offers. EV-volumes has been tracking the developments several years back and gained many useful insights for the impact of incentives and product news.

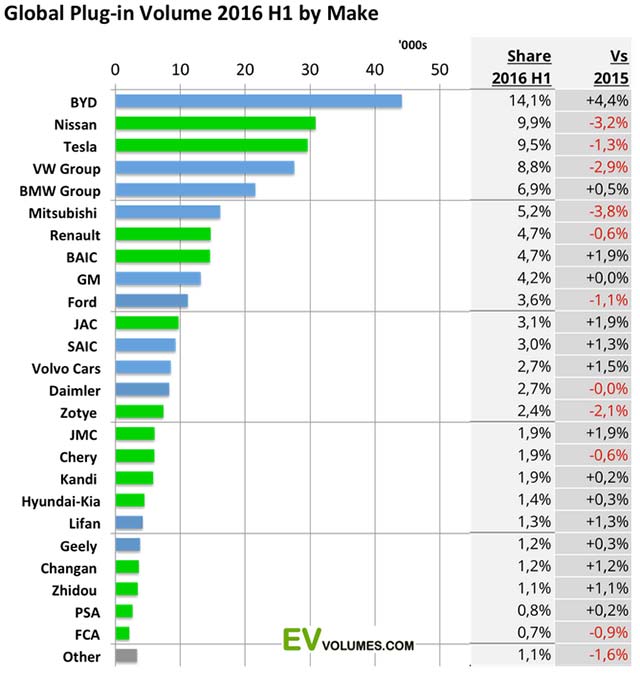

China growth means BYD growth

BYD is the leading make for plug-in vehicles in China. With high volume sales of their 2 PHEVs (Qin, Tang) and 3 EVs (e5, e6, Denza), BYD reached 61 700 sales in 2015, making it the world’s largest OEM for plug-in passenger cars & SUVs. With China being the fastest growing market for plug-ins, BYDs #1 position is affirmed by a wider margin in 2016.

At the end of 2015, the VW Group including Audi and Porsche was on rank #2 with 59 400 sales, Nissan was #3, Tesla #4, Mitsubishi #5. The changes at the top for 2016 are quite considerable with e.g. VW loosing 2 spots vs 2015. Their otherwise leading China operations still struggle to localize plug-in models. Mitsubishi slipped to #6 with aging models and the still pending US intro of the Outlander. Tesla, Nissan and BMW advanced 1 rank.

It has to be pointed out that very few makes (Zotye and Fiat) actually lost volume, compared to 2015 H1. All others increased volume, but in a fast growing market, growing slower means losing share. The +/- % values vs 2015 show the share gains and losses for 2016 H1 compared to 2015 H1.

The common pattern is that nearly all Chinese OEM gained share and most makers outside China lost share. Volvo is a notable exception with a 1,5 % gain, which was not generated in China. The company increased plug-in volume from 2600 to 8500 units for the first half year.

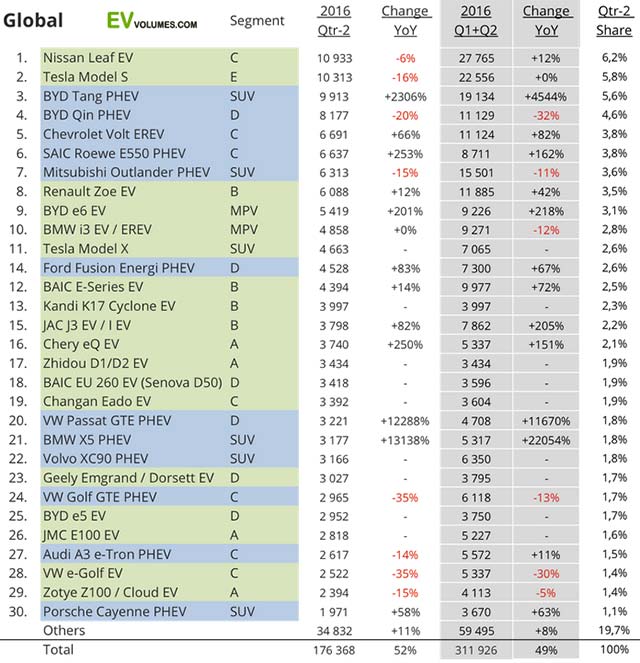

Nissan Leaf back on top

When global sales by model were summed up for the complete 2015 the Tesla Model S came out as the world’s best-selling plug-in vehicle. The Model S is now joined by the Model X (7000 sales this year, nearly all in US and Canada), buy numerous production and supplier problems curbed Tesla’s output from January thru April.

So, despite just 12 % growth for the Leaf this year, it is back on top, for the quarter and Q1+Q2 combined. The ranking is sorted by the Q2 results.

The success story of the BYD Tang PHEV continues with over 19 000 sales during H1 and place 3. Its stablemate, the BYD Qin, is facing stronger competition from upshots like the Roewe E550 PHEV from Shanghai Automotive and diversions from Qin to Tang are likely. The global top 30 list for Q2 contains 15 models form China and 4 of them are in the top-10.

There were many winners and few losers in terms of volumes. Apart from the aforementioned, among the losers were the Mitsubishi Outlander PHEV (NL market), BMW i3 (range upgrade coming) and both VW Golf versions, PHEV and EV.

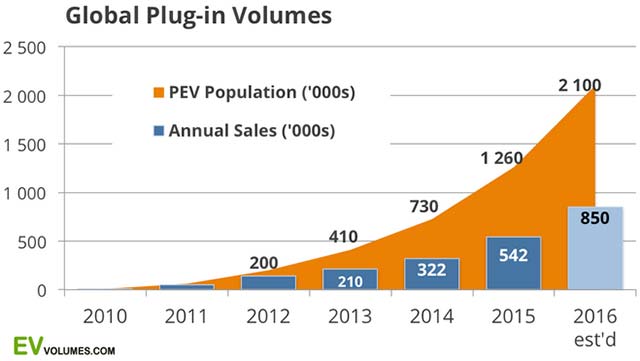

More than 2 million Plug-ins by the end of 2016

The sum-up of the markets indicates a global total of 850 000 units electrically chargeable vehicle sales for 2016. It means 57 % growth over 2015 volumes and a 0,9 % share in the total vehicle market of approximately 92 million units. Plug-in volumes develop slower than desired in Europe and USA, but growth in China makes up for it.

In September 2015, the plug-in vehicle population on the road reached its first million. By December 2016 this number is likely to each 2 million globally. Important milestones, but a lot more needs to happen to reach the ambitious goals for green vehicle deployment established by a number of national governments.

[source: EV-Volumes]